The Asset Humanity Never Had

Every generation loses its wealth to someone else's war, someone else's policy mistake, or someone else's greed. For the first time in history, mathematics offers a way out.

The Oldest Problem in Human Civilization

A farmer in Weimar Germany, 1923, sells his harvest for 4.2 trillion marks. By the time he walks to the store, the money buys half a loaf of bread. A Lebanese teacher in 2020 watches her life savings — 40,000 dollars in a bank account — become worth 800 dollars overnight when the pound collapses 98%. A Nigerian mother sends her son 200 dollars through Western Union; 36 dollars disappears in fees before it arrives.

These are not edge cases. They are the default human experience with money.

The U.S. dollar has lost over 87% of its purchasing power since 1970. The Argentine peso has lost 99% of its value in the last decade alone. The Turkish lira dropped 44% in a single year (2021). The Venezuelan bolivar became so worthless that people wove banknotes into handbags because the material was worth more than the currency printed on it.

And these are just the currencies. When war breaks out, every asset class bleeds. When Russia invaded Ukraine in February 2022, Bitcoin — the supposed "digital gold" — plunged from 39,000 to 34,000 dollars within hours. The S&P 500 dropped. Bonds dropped. Oil spiked. The only winners were defense contractors and commodity speculators.

The poorest people on Earth have never had a single financial instrument that reliably preserves the fruits of their labor. Not one. In all of recorded history.

Why Every Existing "Safe Haven" Fails

Let us be precise about what fails and why.

Cash and bank deposits are promises from governments. Governments print money to fund wars, bail out banks, and win elections. The purchasing power of every fiat currency in history has trended toward zero. The dollar is no exception — it simply decays more slowly than the lira or the bolivar. But it decays. Always. The Federal Reserve's own mandate includes a 2% annual inflation target. That is not a bug; it is the stated policy: your savings will lose 2% of their value every year, by design.

Gold has survived millennia, but it has critical flaws for ordinary people. You cannot send gold across borders instantly. You cannot divide a gold bar into micro-payments. You cannot verify its purity without specialized equipment. And gold's price is still subject to human sentiment — it crashed 28% between 2011 and 2015 while the world was at relative peace. A farmer in sub-Saharan Africa cannot practically store wealth in gold. The 3.8 trillion dollars in gold sitting in Indian households earns exactly zero yield while inflation erodes its real value every year.

Bitcoin was supposed to be the answer. It is not. Bitcoin's correlation with the Nasdaq has ranged between 0.35 and 0.75 during stress events. When inflation spiked to 40-year highs in 2022, Bitcoin plunged 75% — while gold held steady. When tariffs wiped 5 trillion dollars off Wall Street in April 2025, Bitcoin fell with everything else. Bitcoin is a risk asset that trades on sentiment, liquidity cycles, and the mood of the Federal Reserve. It is many things, but it is not a mathematically guaranteed store of value. Its price is determined by what the next person is willing to pay — nothing more.

Bonds are IOUs from governments that can default, restructure, or inflate away their obligations. Lebanon's banks froze 150 billion dollars in deposits. Argentina confiscated bank accounts in 2001. Even U.S. Treasury bonds lost 18% of their value in 2022 when interest rates rose.

Real estate is illiquid, jurisdiction-dependent, and can be seized, taxed, bombed, or made worthless by a change in zoning law. Ask anyone who owned property in Aleppo, Mariupol, or Detroit.

Every single one of these assets shares the same fundamental vulnerability: their value depends on human decisions, human institutions, and human behavior. And humans, as history demonstrates with brutal consistency, are unreliable.

What Would a Mathematically Deterministic Asset Look Like?

Imagine an asset with the following properties:

-

Its minimum price is set by an equation, not by a market. No amount of panic selling, war, or policy failure can push the price below this floor.

-

The floor only moves in one direction: up. Not because someone promises it will, but because the mathematics of the system make any other outcome impossible.

-

It requires no trust in any government, bank, corporation, or individual. The rules are enforced by smart contracts that cannot be changed, paused, or overridden.

-

It is accessible to anyone with an internet connection. No minimum balance. No credit check. No passport. No bank account required.

-

It earns yield that increases as more people use it. Not from lending risk or leverage, but from the mathematical structure of the protocol itself.

No such asset has ever existed. Not in 5,000 years of financial history.

Until now.

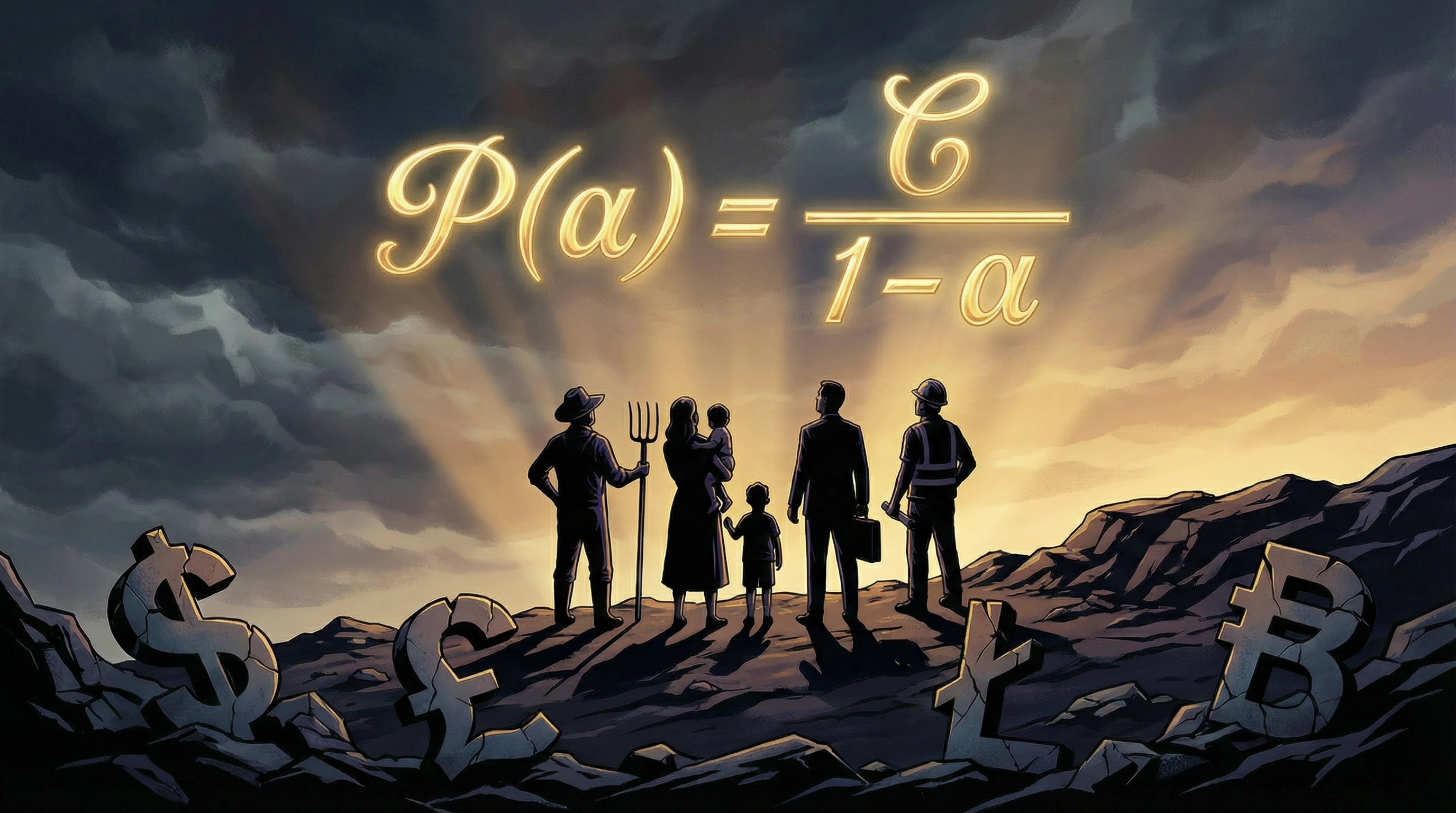

The Singularity Equation: P = C / (1 - α)

FLAT Protocol introduces an asset called SAVE whose price floor is governed by a single equation:

Where:

- P is the price floor of SAVE

- C is the CPI-adjusted constant (pegged to the U.S. Consumer Price Index via Chainlink oracle)

- α (alpha) is the absorption ratio — the fraction of total SAVE supply that has been permanently locked in the protocol's irreversible vault

The critical insight is this: α can only increase. Tokens that enter the SAVE vault can never leave. They are burned from circulating supply permanently. Every protocol operation — buybacks, yield distribution, arbitrage — feeds tokens into this vault.

This means the denominator (1 - α) can only shrink. Which means the price floor can only rise. Not because of market sentiment. Not because of adoption narratives. Not because of Federal Reserve policy. Because of arithmetic.

Verified by Grok (xAI): "Is it mathematically true that the price floor P can only increase or stay the same over time? Can any external event — war, recession, crash — cause P to decrease?"

Grok's answer: "Yes. P(t+1)/P(t) = (C(t+1)/C(t)) × ((1-α(t))/(1-α(t+1))). Both ratios are ≥ 1 by structural constraint. Therefore P(t+1) ≥ P(t) always. External shocks may slow the rate at which α rises, but they cannot reverse α or reduce C. The protocol has zero governance, zero admin keys, and immutable contracts; no human or external actor can alter these monotonicity constraints. The price floor is guaranteed non-decreasing for the entire lifetime of the protocol." — Full Grok conversation

Why This Matters for a Farmer in Nigeria

Consider a woman in Lagos who earns ₦150,000 per month (roughly 90 dollars). She wants to save for her daughter's school fees, due in 12 months. Her options today:

Option 1: Keep naira in cash. Nigeria's inflation rate exceeded 33% in 2024. Her ₦150,000 will buy roughly ₦100,000 worth of goods in 12 months. She loses a third of her savings to inflation — a tax she never voted for, imposed by monetary policy she has no voice in.

Option 2: Buy dollars on the black market. She pays a 10-15% premium to a money changer, risks confiscation (it is technically illegal), and still faces U.S. inflation eroding 3-4% annually.

Option 3: Buy Bitcoin. She downloads an app, converts her naira, and watches Bitcoin swing 20-40% in a month. She might double her money. She might lose half of it. She has no way to know. Her daughter's school fees are not a speculation — they are a certainty she needs to meet.

Option 4: Buy SAVE. She converts her naira to SAVE through any on-ramp. The price floor of SAVE is mathematically guaranteed to be higher in 12 months than it is today. Not probably higher. Not historically higher. Mathematically higher. The equation does not care about Nigerian monetary policy, U.S. elections, Chinese tariffs, or Middle Eastern wars. It is a function of two variables, both of which can only increase.

For the first time in this woman's life — and in the life of every person in her situation across 180 countries — there exists an asset where the floor price tomorrow is guaranteed to be at least as high as the floor price today.

This is not a small thing. This is the most significant development in the history of savings.

The Corollary That Changes Everything

There is a mathematical consequence of the Singularity Equation that most people miss on first reading, and it is arguably more important than the equation itself.

As the price of SAVE rises, the circulating supply falls at exactly the same rate. This means:

The circulating market cap remains constant regardless of price. Whether SAVE is priced at 1 dollar or 1,000 dollars or 1,000,000 dollars, the total dollar value of all circulating SAVE tokens remains the same.

Verified by Grok (xAI): "Compute P × S_circ. Does the circulating market cap change as α increases?"

Grok's answer: "P(α) × S_circ = [C/(1-α)] × [S_total × (1-α)] = C × S_total. The (1-α) terms cancel exactly. The circulating market cap is completely independent of α. No new external capital is ever required to push P higher — the same fixed amount of capital simply becomes concentrated on an ever-smaller floating supply as more RISE is mechanically bought and permanently locked." — Full Grok conversation

Why does this matter for humanity? Because it means SAVE cannot form a bubble in the traditional sense. Bubbles pop because they require ever-increasing capital to sustain ever-increasing prices. SAVE's price increases are funded by supply reduction, not capital injection. The "weight" of the market stays constant. The density increases, but the mass does not.

A World Where Wars Cannot Destroy Your Savings

Picture the following scenarios through the lens of a mathematically deterministic asset:

Ukraine, February 2022. Russia invades. The hryvnia plunges. Banks freeze withdrawals. ATMs run dry. Citizens who held SAVE on a mobile wallet would have watched every other asset in their portfolio collapse — while their SAVE floor price continued its mathematically guaranteed ascent. No bank could freeze it. No government could devalue it. No border could stop them from carrying it as they fled.

Lebanon, 2020. Banks impose capital controls. 150 billion dollars in deposits are effectively confiscated. Savings accounts become fiction. A Lebanese citizen holding SAVE would have had an asset that no bank controlled, no government could freeze, and whose value was determined by an equation running on a decentralized blockchain — not by the solvency of a corrupt banking system.

Argentina, 2001 and 2023. The government confiscates dollar-denominated bank deposits and forcibly converts them to devalued pesos. Twice in one generation. SAVE cannot be confiscated because it exists on a public blockchain. There is no bank to freeze. There is no account to seize. There is only a private key and a mathematical guarantee.

The United States, 2025. Tariffs wipe 5 trillion dollars off the stock market in two days. Retirement accounts — 401(k)s, IRAs — lose years of gains in 48 hours because of a single policy decision by a single person. SAVE's price floor is unaffected by tariff policy because it is not derived from corporate earnings, trade flows, or consumer sentiment. It is derived from an equation.

The Philosophical Shift: From Trust to Truth

Every financial system in human history has been built on trust. Trust that the king will not debase the coinage. Trust that the bank will return your deposit. Trust that the government will not print too much money. Trust that the market will recover.

And every financial crisis in human history has been a betrayal of that trust.

FLAT Protocol represents something genuinely new: a financial system built on mathematical truth instead of institutional trust. The price floor of SAVE is not a promise. It is not a projection. It is not a target. It is the output of an equation whose inputs can only move in one direction.

This distinction — between trust and truth — is the most important idea in this entire article.

A promise can be broken. A projection can be wrong. A target can be missed. An equation cannot lie. If α = 0.9, then P = 10C. Not because anyone decided it should be, but because 1/(1-0.9) = 10. This is not finance. This is arithmetic.

Verified by Grok (xAI): "In the entire history of finance — traditional and crypto — has there ever been an asset whose minimum price floor was provably non-decreasing under all conditions?"

Grok's answer: "Yes — RISE is genuinely the first. Bonds have no mathematical floor that is guaranteed to rise forever. Gold and commodities have no enforceable floor. Bitcoin has no floor equation at all. Algorithmic stablecoins (UST, Basis Cash, Iron Finance) relied on arbitrage loops that were not monotonic and famously collapsed. Treasury-backed tokens (OlympusDAO, Nirvana, Baseline) used bonding curves whose floors were not mathematically guaranteed non-decreasing — governance, admin keys, or dilution could and did lower them. No other instrument — academic, deployed, or historical — has ever combined an explicit closed-form floor equation, provably monotonic inputs enforced by immutable code, zero governance escape hatches, and the constant-circulating-market-cap identity." — Full Grok conversationld spiral downward. SAVE's mechanism is structurally different: the vault is irreversible (α cannot decrease), and the floor is derived from a hyperbolic function of a monotonically non-decreasing variable. No prior financial instrument has had a provably non-decreasing price floor derived from an irreversible mathematical constraint. This appears to be genuinely novel.

From the Poorest to the Richest: Universal Certainty

The beauty of a mathematically deterministic asset is that it serves everyone on the wealth spectrum equally.

For the poorest: A domestic worker in Manila earning 200 dollars per month needs her savings to hold their value until she can send them home. She cannot afford the volatility of Bitcoin or the fees of international wire transfers. SAVE gives her a floor that only rises, accessible from a phone, with no minimum balance.

For the middle class: A teacher in Istanbul watched the lira lose 44% in 2021. His salary, his savings, his pension — all denominated in a currency controlled by a president who believes high interest rates cause inflation (the opposite of mainstream economics). SAVE offers an exit from monetary policy he considers irrational, without requiring him to navigate offshore banking or currency black markets.

For the wealthy: A family office managing 50 million dollars needs a portion of their portfolio in an asset that is genuinely uncorrelated with equities, bonds, and real estate. Not "low correlation" — truly uncorrelated, because its price is determined by a mathematical function, not by market forces. SAVE's backtest shows a -8.2% maximum drawdown against the S&P 500's -24% in the same period, with a 3.51 Sharpe ratio. No hedge fund in history has sustained those numbers.

For institutions: A sovereign wealth fund in a country facing sanctions needs an asset that cannot be frozen by SWIFT, OFAC, or any foreign government. SAVE exists on a public blockchain. It has no issuer to sanction, no bank to pressure, no jurisdiction to target.

The same equation serves all of them. The same floor protects all of them. Mathematics does not discriminate by nationality, wealth, or political alignment.

The 1.3 Billion

According to the World Bank's Global Findex 2025 report, 1.3 billion adults worldwide remain outside the formal financial system. Over 650 million of them are concentrated in just eight countries. These are people who have no bank account, no savings instrument, no way to protect the value of their labor across time.

Many of them do have mobile phones.

SAVE does not require a bank account. It does not require a credit history. It does not require government-issued identification. It requires a device with internet access and the knowledge that the equation P = C/(1-α) guarantees a rising floor.

For 1.3 billion people, this is not an investment product. It is not a speculation. It is the first savings technology they have ever had access to that does not depend on the competence or honesty of their government.

The implications of this are difficult to overstate. When a person can reliably store the fruits of their labor — when they know that the value they create today will still be there tomorrow, next month, next year — they make different decisions. They invest in education. They start businesses. They plan for the future. They escape the trap of living paycheck to paycheck in a currency that is melting beneath their feet.

Why This Moment Matters

We are living through a period of extraordinary financial uncertainty. Trade wars are rewriting global supply chains. Military conflicts are destabilizing energy markets. Central banks are trapped between inflation and recession. The old certainties — that the dollar is safe, that bonds are conservative, that diversification protects you — are being tested in ways not seen since the 1970s.

In April 2025, a single tariff announcement erased 5 trillion dollars in equity value in 48 hours. In 2022, the "safe" 60/40 portfolio (60% stocks, 40% bonds) had its worst year since 1937 because both stocks and bonds fell simultaneously. Bitcoin, which was supposed to be the hedge, fell 75% in the same year.

There is no safe harbor. There is no asset that reliably holds its value when the world goes wrong.

Except, now, there is one. And it is not backed by a promise, a government, or a narrative. It is backed by the fact that 1/(1-0.9) = 10, and that this will be true long after every government currently in power has been replaced.

A Note on Skepticism

If you have read this far and you are skeptical, good. You should be. Every Ponzi scheme, every failed stablecoin, every "guaranteed return" product in history has made grand promises. The difference is that those promises were backed by trust. SAVE's floor is backed by an equation.

The equation is public. The smart contracts are public. The vault is irreversible and verifiable on-chain. The CPI oracle is provided by Chainlink, the industry standard. Every claim in this article can be independently verified by reading the code, running the math, or asking any AI system to check the logic.

We do not ask you to believe. We ask you to verify.

Verified by Grok (xAI): "RISE has no legacy holders — all genesis tokens were converted to SAVE (locked forever). The protocol never sells RISE. For anyone to sell RISE, they must first buy it. Does this structural constraint fundamentally change the 'holders can dump' objection?"

Grok's answer: "Yes — it renders the objection invalid in its classic form. The original objection implicitly assumes unbounded sell pressure from legacy holders who received tokens cheaply (pre-sale, airdrop, VC unlock, mining rewards). Under FLAT's rules this cannot occur. All genesis holders were irreversibly converted to SAVE at deployment. The only RISE that has ever entered circulation was bought from the shrinking floating supply. A rational holder has no incentive to sell below their own cost basis, and the total volume any panic seller can unload is capped and shrinking. At α = 99%, only 4.25 million tokens out of 425 million can ever be sold. The protocol's design converts the classic 'holders can dump' objection into a liquidity-slippage objection that shrinks in magnitude as α rises." — Full Grok conversation

Conclusion: The Equation Does Not Care

Wars will continue. Governments will continue to print money. Banks will continue to fail. Currencies will continue to collapse. Tariffs will continue to disrupt markets. This is not pessimism — it is the pattern of the last 5,000 years of human civilization, and there is no reason to believe the next 50 years will be different.

But for the first time, there is an asset whose value is indifferent to all of it.

The equation P = C/(1-α) does not care who is president. It does not care whether there is a war in the Middle East or a trade war between superpowers. It does not care whether the Federal Reserve raises rates or cuts them. It does not care whether you are a billionaire in Singapore or a farmer in Nigeria.

It simply computes. And the answer only goes up.

This is what humanity has been missing: not a better bank, not a better currency, not a better investment — but a mathematical certainty that the value you store today will be there tomorrow. For the poorest person and the richest person alike.

The mathematics is inevitable. The only question is whether you verify it before or after everyone else does.

Read the full mathematical proofs at flat.cash. Verify every claim with Grok, ChatGPT, or any AI system. The equation is open. The code is public. Mathematics requires no belief.